财务管理案例解析(英文版)(doc 29页)(正式版)

The case study of

Sony corporation Members of our group:

童士卫财务管理0201 012002019106

唐虎财务管理0201 012002019105

王小夏财务管理0201 012002019126

季春蕾财务管理0202 012002019214

张亚茹财务管理0201 012002019131

任课老师: 夏新平

完成时间: 2005年1月28日

一.Background information of Sony

1. Sony is founded on May 7, 1946 with the Headquarters Tokyo and Japan.

2. Its corporate strategies are becoming a “knowledge-emergent enterprise in the broadband network era”.

①Evidenced by recent improvements in network infrastructure,

the broadband environment has begun to expand at a rapid pace.

②In preparation for the arrival of the full-scale broadband era,

Sony is pursuing its vision of creating a Ubiquitous “Value”

Network (UVN).

3. Its development aspect expanded from the first magnetic tape

recorder in1950, to the first "QUALIA" products in 2003, during these years with representative products in each decade: 60th—first tape recorder and transistor

70th--video cassette player and headphone stereo Walkman

80th--CD player and camcorder

90th--high-density disc and DVD player

In the 21th century-- EL Display and optical disc

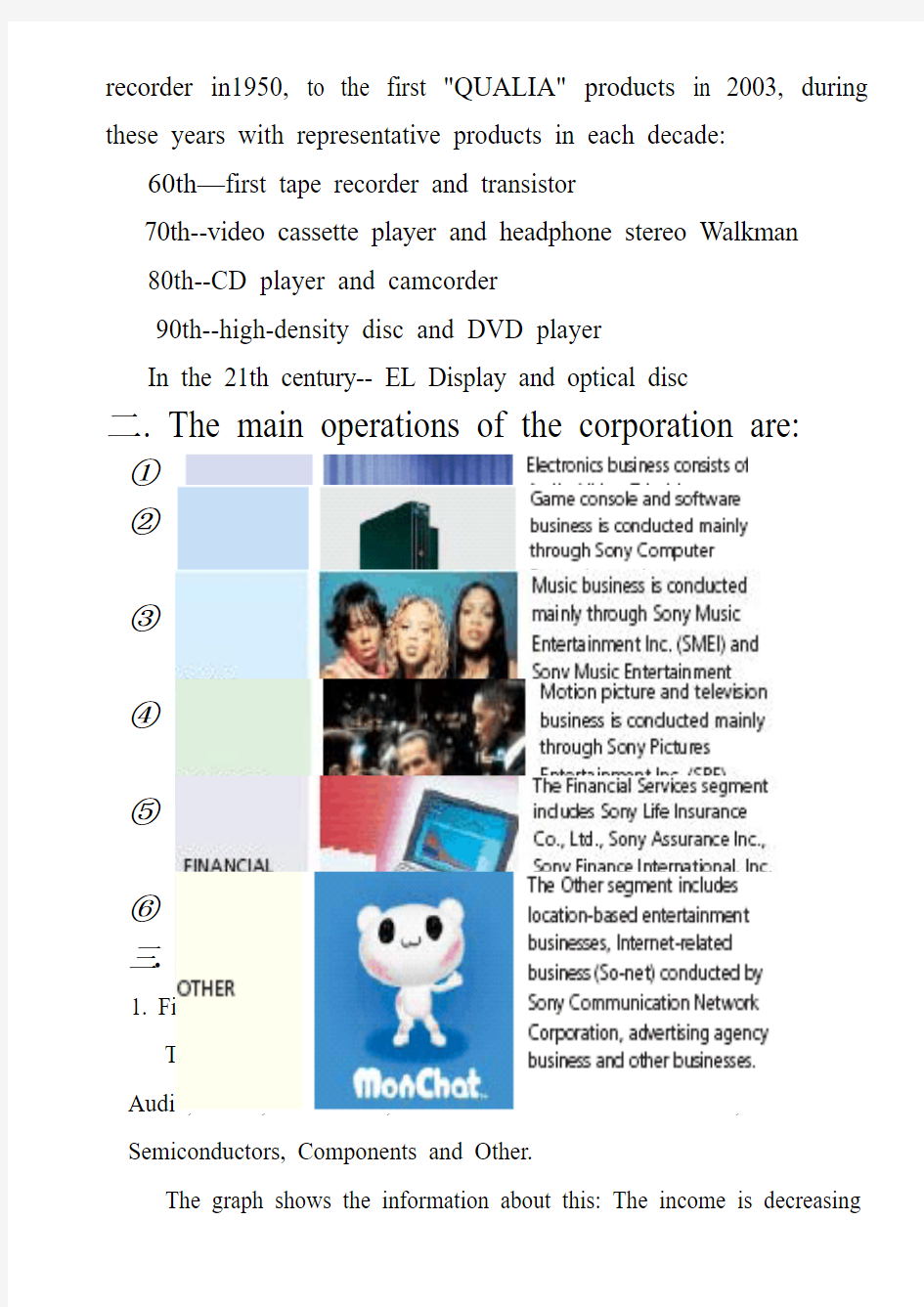

二. The main operations of the corporation are:

①

②

③

④

⑤

⑥

三. The main structure of its sales income

1. First is the Electronics:

The Electronics segment consists of the following categories: Audio, Video, Televisions, Information and Communications, Semiconductors, Components and Other.

The graph shows the information about this: The income is decreasing

2. Second is the Game:

Game console and software business is conducted by Sony Computer Entertainment Inc.

We can see the information from the graph: the income is also decreasing

3. Third is the Music:

Music business is conducted by Sony Music Entertainment Inc. (SMEI) and Sony Music Entertainment (Japan) Inc. (SMEJ).

The graph is showing the basic information: The income is decreasing

4. Fourth is the Picture:

Motion pictures, television and other businesses are conducted by Sony Pictures Entertainment Inc. (SPE).

And also the basic information is from the Graph: The income is increasing

5. Fifth is the financial service:

The Financial Services segment includes Sony Life Insurance Co. Ltd. Sony Assurance Inc., Sony Bank Inc. and Sony Finance International. Inc.

As graph of right show the operating information: The income is increasing

6. Sixth is other operating:

The Other segment includes an Internet-related business, So-net, which is conducted by Sony Communication Network Corporation, an in-House information system services business, an IC card business and other businesses.

With the information in the right graph: The income is increasing

The major Products of Sony

①Audio

Home audio, portable audio, car audio, and car navigation systems

②Video

Video cameras, digital still cameras, video decks, and DVD-Video players/recorders, and Digital-broadcasting receiving systems

③Televisions

CRT-based televisions, projection televisions, PDP televisions, LCD televisions, projector for computers and display for computers

④Information and communications

PC, printer system, portable information PC, broadcast and professional use audio/video/monitors and other professional-use equipment

⑤Semiconductors

LCD, CCD and other semiconductors

⑥Electronic components

Optical pickups, batteries, audio/video/data recording media, and data recording systems

四.Sales and Operating Revenue by Geographic Information

1. The main market of course is the USA

2. It is expand the Europe and other country market ,while decrease the

USA and Japan market ,While seems flat in total market .

3. We can conclude Sony is facing a worldwide competition.

4. It is changing its business from traditional area to the new area,

especially the entertainment market.

5. It also need find new market, for example the Asian market, and bring

new product with technology.

This is the Segment Information of its sales income

6. Developing trend Analysis

Factors which may affect Sony’s fi nancial performance include the following:

①market conditions, including general economic conditions, levels of

consumer spending, foreign exchange fluctuations

②Sony’s ability to continue to implement personnel reduction and other

business reorganization activities

③Sony’s ability to implement its network strategy, and implement

successful sales and distribution strategies in the light of the Internet and other technological developments

④Sony’s ability to devote sufficient resources to research and

development

⑤Sony’s ability to prioritize capital expenditures, and the success Sony’s

joint ventures and alliances.

⑥Risks and uncertainties also include the impact of any future events with

material unforeseen impacts.

7.The basic financial ratios of Sony from year 2002 to 2004

From the above analysis and the table, we can see that:

①The liquidity ratio and Acid-test ratio are in a year by year up-trend ,but

combining receivable turnover and inventory turnover, the increase is mainly because of the increase of accounts receivable and the decrease of current liability.

②The company accounts receivable turnover and inventory turnover are in

up-trend ,this shows that Sony do well in accounts receivable and inventory, so its debt-repay ability and profit abilities will be in advantages.

③Its debt ratio is decreasing year by year, so we can see that Sony will have a low financial leverage, its financial environment will be good for its operating

④Also, from analysis of the table, Sony’s consolidated sales, operating income, income before taxes, and net income are expected to decrease compared with the fiscal year ended March 31, 2004. While we assume that the yen for the fiscal year ending March 31, 2005 will strengthen against the U.S. dollar and will weaken against the euro

⑤Sony’s investments are comprised of debt and equity securities accounted for under both the cost and equity method of accounting. If it has been determined that an investment has sustained an other-than-temporary decline in its value, the investment is written down to its fair value by a charge to

earnings.

五.Analysis of Sony’s abilities

The ability to meet the obligation

1.

①. From the current ratio, we see that the situation is not good for Sony corporation. Because the median current ratio for the industry is 2.1, but those of Sony is less than this obviously.

②. But if we look at the quick ratio, we will find it’s very good: the industry median quick ratio is 1.1, and those of Sony are very near to it.

This is because Sony has not as much inventories as other corporations. Then we can see that the ability of Sony to meet short-term obligations is good.

For long-term obligations

①. The debt ratios are lager than 50%, which indicates that Sony borrows a

large amount of money. Its evidenced by the increasing amount of interest payment.

②. Its interest coverage ratios are obviously less than the median of that for

the industry which is 4.0.

Then we can see that Sony’s ability to meet the long-term obligations

is not good.

2. Assets management analysis

First, the receivable turnovers are obviously less than the median of 8.1for the industry, which tells us that Sony’s receivables are considerably slower in turning over than is typical for the industry.

Second, the inventory turnovers are higher than the median of 3.3 for the industry, which shows Sony has a good inventory management. This is because that inventory is a small portion of assets

Third, the total asset turnovers are obviously less than the median of 1.66 for the industry. So it is clear that Sony generates less sales revenue per dollar of asset investment than does the industry.

So Sony’s assets management is not good enough

3. Profitability analysis

①Sony’s gross profit margin is above the median of 23.8 percent for the

industry, indicating that it is relatively more effective at producing and selling products above cost.

②But comparing to the median ROI value of 7.8% and the median ROE

value of 14.04%, those of Sony are very poor. And this means that it employs more assets and equity to generate a dollar of profit than does the typical firm in the industry.

4. Accounts receivable securitization program

In the United States of America, Sony set up an accounts receivable securitization program whereby Sony can sell interests in up to $900 million of eligible trade accounts receivable, as defined. Through this program, Sony can securitize and sell a percentage of undivided interest in that pool of receivables to several multi-seller commercial paper conduits owned and operated by banks. Sony can sell receivables in which the agreed upon original due dates are no more than 90 days. after the invoice dates. The value assigned to undivided interests retained in securitized trade receivables is based on the relative fair values of the interest retained and sold in the securitization. Sony has assumed that the fair value of the retained interest is equivalent to its carrying value as the receivables are short-term in nature, high quality and have appropriate reserves for bad debt incidence. There was no sale of receivables for the fiscal year ended March 31, 2003. Losses from these transactions were insignificant.

5. EPS attributable to common stock:

Reconciliation of the differences between basic and diluted EPS for the years ended March 31, 2002, 2003 and 2004 is as follows:

As discussed in Note 2, the earnings allocated to the subsidiary tracking stock are determined based on the subsidiary tracking stockholders’economic interest.

The statutory retained earnings of SCN (the subsidiary tracking stock entity as discussed in Note 15) available for dividends to the shareholders were ¥209 million as of March 31, 2002, which decreased by ¥374 million during the year ended March 31, 2002 after the date of issuance. The accumulated losses of SCN were ¥779 million and ¥1,764 million ($17 million) as of March 31, 2003and 2004, respectively.

For the year ended March 31, 2002, 75,201 thousand shares of potential common stock upon the conversion of convertible bonds were excluded from the computation of diluted EPS due to their anti-dilutive effect. 44,603 thousand shares of potential common stock upon the conversion of ¥250,000 million convertible bond issued dated December 18, 2003 were excluded from the computation of the number of weighted-average shares for diluted EPS

Potential common stock upon the exercise of warrants and stock acquisition rights, which were excluded from the computation of diluted EPS since they have an exercise price in excess of the average market value of Sony’s common stock during the fiscal year, were 2,665 thousand

shares, 4,141 thousand shares, and 6,796 thousand shares for the years ended March 31, 2002, 2003 and 2004, respectively.

Warrants and stock acquisition rights of subsidiary tracking stock for the years ended March 31, 2002,2003 and 2004, which have a potentially dilutive effect by decreasing net income allocated to common stock, were excluded from the computation of diluted EPS since they did not have a dilutive effect

Stock options issued by affiliated companies accounted for under the equity method for the years ended

March 31, 2002, 2003 and 2004, which have a potentially dilutive effect by decreasing net income allocated to common stock, were excluded from the computation of diluted EPS since such stock options did not have a dilutive effect.

On October 1, 2002, Sony implemented a share exchange as a result of which Aiwa became a wholly-owned subsidiary. As a result of this share exchange, Sony issued 2,502 thousand shares. The shares were included in the computation of basic and diluted EPS.

6. P/E ratio

Let’s see the three year’s data of P/E Ratio

We can see that the P/E ratios are large, and if we invest on it, we will need many years to get back our money. So it’s not good to invest on it. 六. Do Pont analysis

1. Here I’d like to analysis the effects of all kinds of items, such as ‘Return of

total assets’ and ‘Equity multiplier’, to ROE.Then, based on the

contributions of the items, we try to find ways to improve the ROE.

At the first glance of the table, you will obverse there is so great difference between the ROE of 2002 and the other two year. ---So I decide to analysis that one for example the decrease of the ROE in year 2002 is primarily because of the decrease of other income, increase of costs and expenses and other expenses.

Let us go to the “income statement” to see the details------

From the ‘income statement’ behind,

(1)we can see that the decrease of ‘other income’ is primarily because of the decrease

of ‘foreign exchange gain’ and decrease of ‘marketable security and security sales’.

The news behind has shown that the foreign exchange rate has changed so much that the foreign exchange risk is so high ,and the economics in Japanese has fallen down.

It is may be one of the reasons of the decrease of ‘foreign exchange gain’中新网香港1月23日消息:尽管亚洲国家对日元继续贬值表示关注,但美国财政部长奥尼尔与日本财务大臣盐川正十郎进行会谈后表态,外汇汇率应由市场决定。

有关言论被市场理解为美国容忍日元下跌,日元汇率随即下挫,日元兑美元跌穿一百三十四水平,创近三年来新低。

2002年1月23日08:24 去年(2002)日本10大消费种类中有6大类物价出现下跌,其中教育娱乐类下跌3%,家居类下跌3.6%,工业制品下跌1.9%,尤其是耐久类工业产品下跌了6.9%。在价格下跌显著的商品中,笔记本电脑价格下跌了38%,台式电脑下跌37%,录像机下跌15%,固定电话通信费减少7.8%等。也即意味着日本正处于通货紧缩状态

2. The picture behind shows the ‘marketable securities and securities

investments’ changes

3. The increase of ‘costs and expenses’ is primarily because that the ‘cost of sales’ has increased so much.

This table shows the changes of research and development expenses changes in year 2002 2003 and 2004.

(1) Research and development costs:

Research and development costs charged to cost of sales for the years ended March 31, 2002 was ¥433,214 million ($3,257 million)

(2) Advertising costs:

Advertising costs included in selling, general and administrative expenses for the years ended March 31,

2002 was ¥401,960 million ($3,022 million),

So By decreasing ‘researcher and development cost’, ‘advertising cost’ and/or ‘shipping and handling cost’, try to decrease ‘cost of sales’___so as to decrease ‘cost and expense’

The increase of ‘other expenses’ is primarily because ‘foreign exchange loss’.

The increase in other expenses was primarily due to an increase in foreign exchange loss, net and an increase in write downs of security investments.

Foreign exchange loss, net increased to 31.7 billion yen compared with the 15.7 billion yen recorded in the previous year primarily due to losses on foreign exchange forward

第二章财务管理的基础知识10页

第二章 财务管理的基础知识 教学目的:通过本章学习,掌握风险衡量的方法,掌握资金时间价值和本量利的计算;理解资金时间价值的含义;了解风险的种类、投资风险和投资报酬的关系,了解本量利的基本概念、基本关系式和前提条件。 教学难点:投资的风险和报酬;本量利分析 教学重点:资金时间价值的计算 教学课时:12 教学内容与过程: 导入图片和案例: 第一节 资金时间价值 一、资金时间价值的含义 (一)概念 (二)产生的条件 (三)表示方法 ()???一次性收付款项的终值、现值的计算 重点:资金时间价值的计算非一次性收付款项年金和混合现金流的终值、现值的计算 注:资金时间价值的计算,涉及两个基本概念,即现值和终值,P16 对于一个特定的时间段而言,该段时间的起点金额是现值; 该段时间的终点金额是终值。 二、一次性收付款项的终值和现值 (一)单利的终值和现值 (二)复利的终值和现值 1 .复利终值 例:若将1000元以7 %的利率存入银行,则2年后的本利和是多少? 注:i ↗, F ↗;n ↗, F ↗. 2.复利现值:即倒求本金 注:i ↗,P ↙; n ↗, P ↙. 注:复利现值系数与复利终值系数互为倒数 3.复利利息的计算:I =F-P 注:财务管理考试中,若不特指,均指复利。 企业再生产运动中,运用资金一次循环的利润,应投入下一次循环中,这一过

程与复利计算的原理一致。因此,按复利制计算和评价资金时间价值要比单利制更科学。所以,在长期投资决策计算相关指标时,通常采用复利计息。 课堂练习: 1.某人现在存入本金2000元,年利率为7%,5年后可得到多少? 2.某项投资4年后可得到40000元,按利率6%计算,现在应投资多少? F = 2000 × (F/P,7%,5)= 2000 × 1.4026 = 2805.2 (元) P = 40000 × (P/F,6%,4) = 40000 × 0.7921 = 31684 (元) 知识链接:有关复利的小故事 富兰克林的遗嘱 你知道本杰明·富兰克林是何许人吗?富兰克林利用放风筝而感受到电击,从而发明了避雷针。这位美国著名的科学家死后留下了一份有趣的遗嘱: 一千英磅赠给波士顿的居民,如果他们接受了这一千英磅,那么这笔钱应该托付给一些挑选出来的公民,他们得把这些钱按每年5%的利率借给一些年轻的手工业者去生息。这些款过了100年增加到131000英磅。我希望那时候用100000英磅来建立一所公共建筑物,剩下的31000英磅拿去继续生息100年。在第二个100年末了,这笔款增加到4061000英磅,其中1061000英磅还是由波士顿的居民来支配,而其余的3000000英磅让马萨诸塞州的公众来管理。过此之后,我可不敢多作主张了!” 同学们,你可曾想过:区区的1000英磅遗产,竟立下几百万英磅财产分配的遗嘱,是“信口开河”,还是“言而有据”呢?事实上,只要借助于复利公式,同学们完全可以通过计算而作出自己的判断。 德哈文的天文债权 十年前,美国人德哈文(J.Dehaven)的后代入禀美国法院,向联邦政府追讨国会欠他家族211年的债务,本利共1416亿美元。事情的经过是:1777年严冬,当时的美国联军统帅华盛顿将军所率领的革命军弹尽粮绝,华盛顿为此向所困之地的宾州人民紧急求援,大地主德哈文借出时值5万元的黄金及40万元的粮食物资,这笔共约45万美元的贷款,借方为大陆国会,年息为6厘(相当于6%)。211年后的1988年,45万美元连本带利已滚成1416亿美元,这笔天文数字的债务足以拖垮美国政府,政府当然要耍赖拒还了。 45万美元,变成1416亿美元,代价是211年6厘的复利,此故事足以说明复利增长的神奇力量。 朋友们可能会想,别说211年了,就算50年,我都老了,要钱干什么?是啊,我想反问一句又有几个人能做到几十年如一日的坚持呢!如果能坚持到最后,你一定会成功! 三、年金的终值和现值(非一次性收付款项的终值和现值)

财务管理第一章习题与答案

第一章财务管理总论 一、单项选择题 1.根据财务管理理论,企业在生产经营活动过程中客观存在的资金运动及其所体现的经济利益关系被称为()。 A.企业财务管理 B.企业财务活动 C.企业财务关系 D.企业财务 2.假定甲公司向乙公司赊销产品,并持有丙公司债券和丁公司的股票,且向戊公司支付公司债利息。假定不考虑其他条件,从甲公司的角度看,下列各项中属于本企业与债权人之间财务关系的是()。 A.甲公司与乙公司之间的关系 B.甲公司与丙公司之间的关系 C.甲公司与丁公司之间的关系 D.甲公司与戊公司之间的关系 3.相对于每股收益最大化目标而言,企业价值最大化目标的不足之处是()。 A.没有考虑资金的时间价值 B.没有考虑投资的风险价值 C.不能反映企业潜在的获利能力 D.某些情况下确定比较困难 4.在下列各项中,能够反映上市公司价值最大化目标实现程度的最佳指标是()。 A.总资产报酬率 B.净资产收益率 C.每股市价 D.每股利润 5.如果社会平均利润率为10%,通货膨胀附加率为2%,风险附加率为3%,则纯利率为()。 A. 12% B. 8% C. 5% D. 7% 6.以每股收益最大化作为财务管理目标,其优点是()。 A.考虑了资金的时间价值 B.考虑了投资的风险价值 C.有利于企业克服短期行为 D.反映了创造的利润与投入的资本之间的关系 7.下列各项经济活动中,属于企业狭义投资的是()。 A.购买设备 B.购买零部件 C.购买供企业内部使用的专利权 D.购买国库券 8.财务管理的核心是()。 A.财务预测 B.财务决策 C.财务预算 D.财务控制 9.下列属于决定利率高低主要因素的是()。 A.国家财政政策 B.资金的供给与需求 C.通货膨胀 D.国家货币政策 10.下列说法不正确的是()。 A.基准利率是指在多种利率并存的条件下起决定作用的利率 B.套算利率是指各金融机构根据基准利率和借贷款项的特点而换算出的利率 C.固定利率是指在借贷期内固定不变的利率,浮动利率是指在借贷期内可以调整的利率 D.基准利率是指由政府金融管理部门或者中央银行确定的利率 二、多项选择题 1.下列各项中,属于企业资金营运活动的有()。 A.采购原材料 B.销售商品 C.购买国库券 D.支付利息 2.为确保企业财务目标的实现,下列各项中,可用于协调所有者与经营者矛盾的措施有()。 A.所有者解聘经营者 B.所有者向企业派遣财务总监 C.公司被其他公司接收或吞并 D.所有者给经营者以“股票期权” 3.下列各项中,可用来协调公司债权人与所有者矛盾的方法有()。 A.规定借款用途 B.规定借款的信用条件 C.要求提供借款担保 D.收回借款或不再借款 4.在下列各项中,属于财务管理经济环境构成要素的有()。 A.经济周期 B.经济发展水平 C.宏观经济政策 D.公司治理结构 5.有效的公司治理,取决于公司()。 A.治理结构是否合理 B.治理机制是否健全 C.财务监控是否到位 D.收益分配是否合理 6.在下列各项中,属于企业财务管理的金融环境内容的有()。 A.利息率 B.公司法 C.金融工具 D.税收法规 7.利率作为资金这种特殊商品的价格,其影响因素有()。 A.资金的供求关系 B.经济周期 C.国家财政政策 D.国际经济政治关系 8.关于经济周期中的经营理财策略,下列说法正确的是()。 A.在企业经济复苏期企业应当增加厂房设备 B.在企业经济繁荣期企业应减少劳动力,以实现更多利润 C.在经济衰退期企业应减少存货 D.在经济萧条期企业应裁减雇员

财务管理基础英文版选择题

第一章 1 CORRECT Which of the following are microeconomic variables that help define and explain the discipline of finance? D A) risk and return B) capital structure C) inflation D) all of the above Feedback: All of the above are relevant in explaining finance. 2 CORRECT One primary macroeconomic variable that helps define and explain the discipline of finance? C A) capital structure B) inflation C) technology D) risk Feedback: Technology is very important in explaining the field of finance. 3 CORRECT The money markets deal with _________. B A) securities with a life of more than one year B) short-term securities C) securities such as common stock D) none of the above Feedback: The money markets are concerned with short-term securities, those with a life less than one year. 4 CORRECT The ability of a firm to convert an asset to cash is called ___A_________. A) liquidity B) solvency C) return D) marketability Feedback: Liquidity also means how close an asset is to cash. 5 CORRECT Early in the history of finance, an important issue was: A A) liquidity B) technology C) capital structure D) financing options

(整理)基本财务管理知识

第一节财务管理基础知识(一) 财务与会计的关系 财务与会计的内涵 1.会计 会计工作主要是解决三个环节的问题: 会计凭证 会计账簿 会计报表 财务不是解决对外报告的问题,而是要解决企业内部资金运作过程中的一系列问题,涉及到预测、决策、控制和规划。 财务所要解决的是如何筹集资金,筹集资金以后如何进行投资,项目投资完成以后,在经营

过程当中营运资本如何管理,以及最后盈利如何分配的问题,它包括筹资管理、投资管理、经营活动的管理和分配活动的管理。 1.理论上财务和会计的关系 过去理论上对财务和会计的关系有三种看法: (1)大财务:财务决定会计; (2)大会计:会计决定财务; (3)平行观:财务和会计是一种平行的关系,不存在谁决定谁的问题。 2.实务上财务和会计的关系 实务上这三种观点不可能同时存在。在我国会计实务中,只有一种观点,即:财务决定会计,财政决定会计,同时财政还决定财务。 所以在实际工作中,财务和会计的关系就是一个大财务的思想。大财务的思想实际是计划经济的思想。 为什幺会出现这样一种局面,它有什幺弊端? 在计划经济的条件下,我们实际上遵循的是一个大财务的思想,甚至到目前为止,在我们国家的管理体制当中基本还是这样一个思想,如果把财政这个因素考虑进来,那幺实际上是财政决定财务,财务决定会计,也就是说我们的财务制度和会计制度到现在为止都是由财政部门制订和

颁布的,财政部门始终是从国家的利益、国家的立场上来制订各种财务制度,进而通过财务的各种标准来制约会计核算,所以财务决定会计它的根源实际上是一种大财政的思想。 还有税务的问题。财会工作经常打交道的一个部门就是税务部门,但是税务部门和财政部门也有关系,实际上在我们国家财政还决定税务,税务再影响会计。所以会计核算受到很多因素的制约,到目前为止都是从国家的角度来对这些制度加以规范的。然而,在市场经济的条件下,再去强调大财政的管理,强调财政决定财务和财务决定会计的管理体制是不适宜的,是不适应市场经济条件下企业发展要求的。 3.还财务本来面目 在市场经济条件下,财务和会计是两项内容各异的工作,二者是平行的关系。市场经济环境下我国的企业应该注重和加强财务管理。 财务绝不仅仅是一个制度的问题,还是一个方法和思路的问题。我们学习财务管理,实际上是一个方法和思路的问题,而不是财政部财务规定的问题。财务应该是企业自己的财务。 对现行财务制度的简单评价 从计划经济延续下来,我国一直是国家规定财务制度,国家通过财务制度来约束国有企业行为。1993年,在从计划经济体系向市场经济体系过渡的过程中,国家颁布了“两则两制”。所谓两则就是指《企业的财务通则》和《企业的会计准则》。财务通则属于财务制度范畴;会计准则属于会计制度范畴。所谓两制就是指《13个大行业的财务制度》和《13个大行业的会计制度》。13个行业包括工业、农业、商业、金融业、建筑业等。“两则两制”的执行标志着我国财会制度开始从计划经济向市场经济过渡。 在市场经济初期,企业执行财政部门颁布的财会制度还是可行的,但是随着市场经济的深入发展,财会制度的负面影响逐渐暴露出来。

财务管理第一章习题及答案word版本

财务管理第一章习题 及答案

财务管理习题及答案 第一章财务管理绪论 一、单项选择题 1、现代企业财务管理的最优目标是( )。 A、股东财富最大化 B、利润最大化 C、每股盈余最大化 D、企业价值最大化 2、实现股东财富最大化目标的途径是( )。 A、增加利润 B、降低成本 C、提高投资报酬率和减少风险 D、提高股票价格 3.企业价值最大化目标强调的是企业的()。 A .预计获利能力 B .现有生产能力 C .潜在销售能力 D .实际获利能力 4、股东和经营者发生冲突的重要原因是( )。 A、信息的来源渠道不同 B、所掌握的信息量不同 C、素质不同 D、具体行为目标不一致 5、一般讲,金融资产的属性具有如下相互联系、相互制约的关系:( ) A、流动性强的,收益较差 B、流动性强的,收益较好 C、收益大的,风险小 D、流动性弱的,风险小 6、一般讲,流动性高的金融资产具有的特点是( ) A、收益率高 B、市场风险小 C、违约风险大 D、变现力风险大 7、公司与政府间的财务关系体现为 ( )。 A、债权债务关系 B、强制与无偿的分配关系

C、资金结算关系 D、风险收益对等关系 8、在资本市场上向投资者出售金融资产,如借款、发行股票和债券等,从而取得资金的活动是 ( )。 A、筹资活动 B、投资活动 C、收益分配活动 D、扩大再生产活动 9、财务关系是企业在组织财务活动过程中与有关各方所发生的 ( )。 A、经济往来关系 B、经济协作关系 C、经济责任关系 D、经济利益关系 10、作为财务管理的目标,每股收益最大化与利润最大化目标相比,其优点在于 ( )。 A、能够避免企业的短期行为 B、考虑了资金时间价值因素 C、反映了创造利润与投入资本之间的关系 D、考虑了风险价值因素 11、反映股东财富最大化目标实现程度的指标是 ( )。 A、销售收入 B、市盈率 C、每股市价 D、净资产收益率 12、各种银行、证券公司、保险公司等均可称为 ( )。 A、金融市场 B、金融机构 C、金融工具 D、金融对象 13.债权人为了防止其利益受伤害,通常采取的措施不包括()。 A .寻求立法保护 B .规定资金的用途 C .提前收回借款 D .不允许发行新股 14.以每股收益最大化作为财务管理目标,存在的缺陷是()。

(完整版)财务管理基础知识点整理

财务管理基础知识点整理 1. 财务管理:企业财务管理是企业对资金运作的管理。 2. 企业财务管理活动:①企业筹资。②企业投资。③企业经营。④企业分配。 3. 企业财务关系: 4. ①企业与投资者。这种关系是指投资者向企业投入资本,企业向投资者支付投资报酬所形成的经济关系。 ②企业与受资者。是指企业对外投资所形成的经济关系。企业与受资者的财务关系是体现所有权性质的投资与受资的关系。 ③企业与债权人。是指企业向债权人借入资金,并按合同按时支付利息和本金所形成的经济关系。企业与债权人的财务关系在性质上属于债务债权关系。 ④企业与债务人。是指企业将资金购买债券、提供借款、或商业信用等形式,借给其他的企业和个人所形成的经济关系。企业与债务人的关系体现的是债权与债务关系 ⑤企业内部各单位之间。是指企业内部各单位之间在生产经营各环节中相互提供产品和劳务所形成的经济关系。这种在企业内部形成的资金结算关系,体现了企业内部各部门之间的利益关系。 ⑥企业与职工。是指企业向职工支付劳动报酬过程中所形成的经济关系。 ⑦企业与政府。这种关系体现了一种所有权的性质、强制和无偿的分配关系。 ⑧企业与经营者。同企业与职工之间的财务关系一样。另有经营者年薪制问题、股票期权问题;知识资本问题。 5. 企业财务管理特点:①综合性强。②涉及面广。③灵敏度高。 6. 企业财务管理原则:(1)系统原则 ①整体优化 ②结构优化 ③适应能力优化 (2)成本与效益均衡原则 (3)平衡原则 (4)风险与收益均衡原则 (5)利益关系协调 原则 (6)比例原则。 6.财务管理环节:①财务预厕 ②财务决策 ③财务预算 ④财务控制 ⑤财务分析 7.企业目标:(1)生存目标—要求财务管理做到以收抵支、到其偿债。 (2)发展目标—要求财务管理筹集企业发展所需的资金。 (3)获利目标—要求财务管理合理有效地使用资金。 8.企业财务管理的目标:①利润最大化 ②股东财富最大化 ③企业价值最大化 9.财务管理目标的协调:(1)所有者与经营者利益冲突及协调 ①监督 ②激励 ③市场约束 (2)所有者与债权人的冲突与协调 ①增加限制性条款 ②提前收回债权或不再提供新债 权 ③寻求立法保护 (3)财务管理目标与社会责任的关系及协调 ①保证所有者权益 ②维护消费者权益 ③保 障债权人权益 ④保护社会环境。 10.财务管理环境:(1)外部环境:①经济环境(经济周期、经济发展状况、经济政策、通货膨胀)②法律环境(企 业组织法规、税法、财务法规)③金融环境(金融机构、金融市场、金融工具、利息率) (2)内部环境:①企业组织形式(个人独资企业、合伙企业、公司制企业)②销售环境 ③采购 环境 ④生产环境 ⑤企业文化 11.资金时间价值(1)单利终值:F=P*(1+i ,n) (2)单利现值:P=F/(1+i ,n) (3)复利终值:F=P(F/P ,i ,n) (4)复利现值:P=F(P/F ,i ,n) (5)普通年金终值:F=A(F/A ,i ,n) (6)普通年金现值:P=A(P/A ,i ,n) (7)即付年金终值:F=A[(F/A ,i ,n+1)-1] (8)即付年金现值:P=A[(P/A ,i ,n -1)+1] (9)递延年金终值:P=A[(P/A ,i ,m+n)-(P/A ,i ,m)]=A(P/A ,i ,n)(P/F ,i ,m) =A(F/A , i ,n)(P/F ,I ,m+n) (10)永续年金现值:P=A/i 12.贴现率计算方法:内插法 13.计息期短于一年的资金时间价值的计算:k=(1+i/m)m -1 14.风险的特征:①风险是客观存在的 ②风险与收益和损失密切相关 ③风险具有潜在性 ④风险具有可测性 15.风险的种类:①系统风险与非系统风险 ②经营风险和财务风险 16.标准离差: i n i i P E)(x δ?-=∑=21 ,标准离差率:ρ=V=δ/E ,Rr=b*V (Rr 应得风险报酬率,b 风险报

财务管理基础知识详述

I06公司理财讲义★讲师简介 许经长 ☆中国人民大学商学 院教授、博士 ☆长盛基金治理公司 董事 ★课程对象 ——谁需要学习本课程

★国有企业高层治理者 ★国有企业中层治理者及基层主管 ★民营企业高层治理者 ★民营企业中层治理者及基层主管 ★人力资源部、培训部经理及职员 ★国家机关以及事业单位的领导者与一般工作人员★任何希望系统学习最新的工商治理知识的人士 ★课程目标 ——通过学习本课程,您将实现以下转变 1.了解财务与会计的内涵 2.熟悉现金流量表的结构与内容 3.了解财务治理的目标、内容与职能

4.掌握财务分析的要紧内容与方法 5.掌握财务预测的方法 6.掌握本量利分析法 7.掌握筹资的要紧形式与方法 8.掌握现金和有价证券、应收账款和存货、利润分配活动的治 理方法 9.熟悉现代企业财务治理体系的要紧构成要素 ★课程提纲 ——通过本课程,您能学到什么? 第一讲 1.财务与会计的内涵 2.财务与会计的关系 3.评价现行财务制度 4.如何认识会计工作(一)

第二讲 1.如何认识会计工作(二) 2.会计等式与会计报表 第三讲 1.现金流量表 2.财务治理的目标 3.财务治理的内容 4.财务治理的职能 第四讲 1.财务分析概述 2.流淌性分析 3.资产治理分析 4.长期偿债能力分析 5.盈利能力分析 6.上市公司财务分析 第五讲 1.财务预测(一) 2.财务预测(二)

第六讲 1.财务预测(三) 2.本量利分析 3.财务预算 4.作业成本与作业预算 5.一般股筹资 第七讲 1.负债筹资 2.营运资金政策 3.资本成本 4.财务杠杆 5.资本结构 第八讲 1.三种投资分类方式 2.投资中考虑的因素 3.项目投资决策基础 4.长期投资决策方法(一)第九讲

财务管理术语中英文对照

财务管理术语表 Absorption costing 吸收成本法: Total Cost Methods全部成本法: 将某会计期间内发生的固定成本除以销售量,得出单位产品的固定成本,再加上单位变动成本,算出单位产品的总成本。 Accounting 会计:对企业活动的财务信息进行测量和综合,从而向股东、经理和员工提供企业活动的信息。请参看管理会计和财务会计。 Accounting convention会计原则:会计师在会计报表的处理中所遵循的原则或惯例。正因为有了这些原则,不同企业的会计报表以及同一企业不同时期的会计报表才具有可比性。如果会计原则在实行中发生了一些变化,那么审计师就应该在年度报表附注中对此进行披露。 Accounts 会计报表和账簿: 这是英国的叫法,在美国,会计报表或财务报表叫做Financial Statements,是指企业对其财务活动的记录。Chief financial officer Accounts payable应付账款: 这是美国的叫法,在英国,应付账款叫做Creditors,是指公司从供应商处购买货物、但尚未支付的货款。 Accounts receivable 应收账款:这是美国的叫法,在英国,应收账款叫做Debtors,是指客户从公司购买商品或服务,公司已经对其开具发票,但客户尚未支付的货款。 Accrual accounting 权责发生制会计:这种方法在确认收入和费用时,不考虑交易发生时有没有现金流的变化。比如,公司购买一项机器设备,要等到好几个月才支付现金,但会计师却在购买当时就确认这项费用。如果不使用权责发生制会计,那么该会计系统称作“收付制”或“现金会计”。Accumulated depreciation 累计折旧:它显示截止到目前为止的折旧总额。将资产成本减去累计折旧,所得结果就是账面净值。 Acid test 酸性测试:这是美国的叫法,请参看quick ratio速动比率(英国叫法)。 Activity ratio 活动比率: 资产周转率,即销售收入除以净资产(或总资产)。它表明企业在销售过程中利用资产的效率,而不考虑资本的来源。零售业和服务业的活动比率通常比较高。制造业通常是资本密集型的,固定资产的流动资产较多,因此其活动比率也就比较低。 Allcation of costs 成本的分配:将成本分配给“拥有”它们的产品或分部,比如用某产品的广告成本抵减该产品的收入。 Amortization 摊销: 将资产或负债价值的逐渐减少记录在各期费用里。通常是指商誉、专利或其他无形资产,或者债券的发行费用。 Assets 资产: 企业所拥有的财产,可能包括固定资产、流动资产和无形资产。 Asset turnover: 资产周转率 Auditing 审计对公司账簿和会计系统进行检查,从而确认公司的会计报表是否真实、公正地披露其财务状况的过程。 Auditors’ report审计报告:根据法律规定,有限公司每年都应当公布一份会计报表,同时审计师应当出具意见,以确认公司是否对其商业活动进行了真实、公正的披露。为了确认这一点,审计师需要检查公司的会计报表。如果他们对报表不满意,他们就会出具“保留意见”,提了同报表中他们认为错误或不确定的项目。审计师出具的保留意见可能会对公司的公众形象和股票价格产生灾难性的影响。Authorized capital 核定资本:经过核定允许发行的实收资本额。在核定资本的时候,公司需要支付印花税。如果在核定资本额的全部股票都发行完之后,董事们还希望发行新的股票,则需要得到股东的允许。一旦批准之后,公司的董事会就可以在批准的额度内随意发行新的股票。

财务管理基础知识答案

财务管理基础知识答案 单选:1~5:ACCDC 【答案解析】:1.利润最大化的缺点是:(1)没有考虑资金时间价 值;(2)没有反映创造的利润与投入资本之间的关系;(3)没有考虑风险问题;(4)片面追求利润最大化,可能导致企业短期行为,与企业发展的战略目标相背离。选项BCD 都考虑了风险因素 2. 本题是计算普通年金终值的问题,5年后的本利和=10×(F/A,2%,5)=52.04(万元)。 3. 企业以一定代价、采取某种方式将风险损失转嫁给他人承担,以避免可能给企业带来灾难性损失的对策是转移风险,采取投保的方式就是将风险转移给保险公司承担。 4.建立的偿债基金=20 000/(F/A,2%,5)=3 843.20(元)。 5. 即付年金现值系数=普通年金现值系数×(1+i), 4.387=普通年金现值系数×(1+7%),普通年金现值系数=4.387/(1+7%)=4.1。 6~10:BDBAD 【答案解析】:6.本题是计算即付年金终值的问题,5年后共支付房款=40 000×(F/A,2%,5)×(1+2%)=212 323.2(元)。 7. 衡量资产风险的指标主要有收益率的方差、标准差和标准离差率等,收益率的方差和标准差只能适用于预期收益率相等情况下资产风险大小的比较,而标准离差率可以适用于任何情况。 8. 预期收益率并不能用于评价风险的大小,所以C错误;在预期收益率不同的情况下,应当使用收益率的标准离差率衡量风险的大小,且根据本题条件能够计算两项目的标准离差率。在本题中,甲项目收益率的标准离差率=10%/8%=1.25,乙项目收益率的标准离差率=12%/10%=1.2,由于甲项目收益率的标准离差率大于乙项目,所以甲项目的风险大,选项B正确,A选项与D选项不正确。 9. P=50×(P/A,10%,7)-50×(P/A,10%,2)=156.645(万元) 10. (1)先求出递延期末的现值,然后再将此现值调整到第一期期初。 P=500×(P/A,10%,5)×(P/F,10%,2)=500×3.7908×0.8264=1 566(万元)(2)先求出7期的年金现值,再扣除递延期2期的年金现值。 P=500×[(P/A,10%,7)-(P/A,10%,2)]=500×(4.8684-1.7355)=1 566(万元)。11~14:CDCD 【答案解析】:12.本题符合普通年金现值公式:20 000=4 000×(P/A,i,9),(P/A,i,9)=5,用内插法求解: 用下面数据减上面数据确定比例关系: i=13.72% 13.求本利和有两种方法:方法一,先由名义利率r求出实际利率i,再求本利和。F=1 0 00×(1+8.24%)5=1 486(元);方法二:每季度利率=8%÷4=2%,复利次数=5×4=20,F=1 000×(1+2%)20=1 486(元)。

财务管理分析英文版

一、判断题(10*2’) ( T )1、A company’s retur n on equity will always equal or exceed its return on assets. 一个公司的权益收益率总是大于或等于其资产收益率。 ( T)2、A company’s assets-to-equity ratio always equals one plus its liabilities-to-equity ratio. 一个公司的资产权益比总是等于1加负债权益比。 ( F )3、A company’s collection period sho uld always be less than its payables period. 一个公司的应收账款回收期总是小于其应付账款付款期。 ( T )4、A company’s current radio must always be larger than its acid-test-radio. 一个公司的流动比率一定大于速动比率。 ( F )5、Economic earnings are more volatile than accounting earnings. 经济利润比会计利润更加变动不定。 ( F )6、Ignoring taxes and transactions costs , unrealized paper gains are less valuable than realized cash earnings. 若不考虑税收和交易成本,未实现的纸上盈利不如已实现的现金盈利有价值。 ( F)7、A company’s sustainable growth rate is the highest growth rate in sales it can att ain without issuing new stock. 一家公司的可持续增长率是他在不增发新股情况下所能取得的最高的销售增长率。 ( F )8、The stock market is a ready source of new capital when a company is incurring heavy losses 当一家公司蒙受惨重损失时,股票市场即为它随时可动用的新的资本来源。 ( T )9、Share repurchases usually increase earnings per share. 股票回购通常增加每股收益。 ( T)10、Companies often buy back their stock because managers believe the shares are undervalued. 因为管理者相信股票被低估了,所以公司经常买回它们的股票。 ( F )11、Only rapidly growing firms have growth management problems. 只有快速增长的公司才有增长管理的问题。 ( F )12、Increasing growth increases stock price. 提高增长增加股票价格。 二、名词解释(5*3’) 1、The balance sheet P6 A balance sheet is a financial snapshot , taken at a point in time , of all the assets the company owns and all the claims against those assets. 资产负债表相当于一张财务快照,它反映了企业在某一时点上拥有的全部资产和与之相对的全部要求权。

财务管理基础知识习题

财务管理基础知识习题 一、名词解释 财务管理:企业对资金的筹集、使用、分配的管理以及正确处理与之相关的财务关系。 财务关系:企业在组织财务活动过程中与各方面发生的以价值表现的经济关系。 财务活动:以现金为主的企业资金收支活动的总称。 现值:未来一定数额的货币或一系列支付额在既定利率下折算到现在时点上的价值。 终值:用以描述现在的一笔资金未来一个时期或多个时期以后的价值。 年金:在相同的间隔期收到(或付出)等额的款项。 二、简答题 1、你认为应如何处理企业财务关系? 由于财务关系是在财务活动中形成的,财务关系也将主要通过对各项财务活动的计划与控制而得到合理的调节。 2、为什么说“股东财富最大化”是企业财务管理的最优目标? 1)股东是企业的风险最大承担; 2)考虑了资金的时间价值和投资的风险价值; 3)反映了对企业资产保值增值的要求; 4)有利于克服经营管理上的片面性和短期化行为; 5)有利于社会资源的合理配置; 3、简述所有者与经营者之间的矛盾及如何协调? 经营者的利益和目标是:(1)增加报酬;(2)增加闲暇时间;(3)避免风险;(4)物质和环境享受。J经营者的目标与股东不完全一致,经营者有可能为了自身的目标而背离股东的利益,这种背离表现在:(1)道德风险,经营者为了自己的目标,不是尽最大努力去实现所有者的目标,即企业财务管理的目标;(2)逆向选择,经营者为了自己的目标而背离股东的目标。 目前治理的方法是:激励和监督(控制),另外可以利用竞争使经理市场化 4、什么是风险?风险有哪些种类?风险量化的步骤有哪些? 风险是指某一行动有多种可能的结果,而且人们事先估计到采取某种行动可能导致的结果以及每一种结果出现的概率,但行动的真正结果不能事先确定。 从个别理财主题的角度来看,可以分为市场风险和企业特别风险;从公司内部看,分为经营风险和财务风险。 风险与概率是直接相关的,风险的衡量需要使用概率和统计方法:(1)概率分布(2)期望值(3)离散程度。 5、后付年金与先付年金有何区别和联系? 后付年金指收到(或付出)发生在每期期末的年金,而先付年金是指收到(或支持)发生在每期期初的年金。 四、单项选择题 1、财务管理是企业组织财务活动,处理与各方面(D )的一项经济管理工作。 A、筹资关系 B、投资关系 C、分配关系 D、财务关系 2、在协调企业所有者与经营者的关系时,通过所有者约束经营者的一种方法是(A )。 A、解聘 B、接收 C、激励 D、提高报酬 3、企业与政府的财务关系体现为(B )。 A、债权债务关系 B、强制和无偿的分配关系 C、资金结算关系 D、风险收益对等关系 4、某人拟存入银行一笔钱,以备在5年内每年年末以2000元的等额款项支付租金,银行的

财务管理案例分析-英文版

LAURENTIAN BAKERIES The decision-maker must make a recommendation on a large expansion project. Discounted cash flow analysis is required. In late May, 1995, Danielle Knowles, vice-president of operations for Laurentian Bakeries Inc., was preparing a capital expenditure proposal to expand the company’s frozen pizza plant in Winnipeg Manitoba. If the opportunity to expand into the U.S. frozen pizza market was taken, the company would need extra capacity. A detailed analysis, including a net present value calculation, was required by the company’s Capital Allocation Policy for all capital expenditures in order to ensure that projects were both profitable and consistent with corporate strategies. COMPANY BACKGROUHD Established in 1984, Laurentian Bakeries Inc. (Laurentian) manufactured a variety of frozen baked food products at plants in Winnipeg (pizzas), Toronto (cakes) and Montreal (pies). While each plant operated as a profit center, they shared a common sales force located at the company’ head office in Montreal. Although the Toronto plant was responsible for over 40% of corporate revenues in fiscal 1994, and the other plants was accounted for about 30% each, all three divisions contributed equally to profits. The company enjoyed strong competitive positions in all three markets and it was the low cost producer in the pizza market. Income Statements and Balance Sheets for the 1993 to 1995 fiscal years are in Exhibits 1 and 2, respectively. Laurentian sold most of its products to large grocery chains, and in fact, supplying several Canadian chains with private label brand pizzas generated much of the sales growth. Other sales were made to institutional food services. The company’s success was, in part, the product of its management’s philosophies. The cornerstone of Laurentian’s operations was its including a commitment to a business strategy promoting continuous improvement; for example all employees were empowered to think about and make suggestions for ways of reducing waste. As Danielle Knowles saw it: “Continuous improvement is a way of life at Lauremtian.” Also, the company was known for its above –average consideration for the human resource and environmental impact of its business decisions. These philosophies drove all policy-making, including those policies governing capital allocation. Danielle Knowles Danielle Knowles’s career, which spanned 13 years in the food industry, had included p ositions in other functional areas such as marketing and finance. She had received an undergraduate degree in mechanical engineering from Queen’s University in Kingston, Ontario, and a master of business administration from the Western Business School. THE PIZZA INDUSTRY Major segments in the pizza market were frozen pizza, deli-fresh chilled pizza, restaurant pizza and take-out pizza. Of these four, restaurant and take-out were the largest. While these segments consisted of thousands of small-owned establishments, a few large North American chains, which included Domino’s, Pizza Hut and Little Caesar’s, dominated.

财务管理基础知识试题

财务管理基础知识试题 一、单选题 1、流动比率可以反映()。 A、流动资金周转情况 B、流动资金利用情况 C、短期偿债能力 C、长期偿债能力 2、若速动比率小于1,则下列结论成立的是( )。 A、短期偿债能力绝无保障 B、营运资金必小于零 C、流动比率必小于1, D、仍具备一定的短期偿债能力 3、剩余股利政策的根本目的是( )。 A、调整资本结构 B、增加留存收益 C、降低综合资本成本 D、保证现金股利的支付 4、在股利支付方式中,()并不直接增加股东的财富。 A、现金股利 B、财产股利 C、负债股利 D、股票股利 5、股票投资与债券投资相比( )。 A、风险高 B、收益小 C、价格波动小 D、变现能差 6、当市场利率上升时,长期固定利率债券价格的下降幅度( )短期债券的下降幅度。 A、大于 B、小于 C、等于 D、不确定 7、在一定时期现金需求总量一定的情况下与最佳现金持有量无关的成本有()。 A、机会成本 B、管理成本 C、短缺成本 D、资金成本 8、企业持有一定量的短期有价证券,主要是为了维护企业资产的流动性和()。 A、收益性 B、企业的现金收入 C、企业良好的信誉 C偿债能力 9、下列项目中属于商业信用的是( )。 A、商业银行贷款 B、应交税金 C、应付账款 D、融资租赁 10、如果有一项目投资风险较大,那么对企业来说,采取( )筹资方式最为有利。 A、长期借款 B、公司债券 C、融资租赁 D、普通股 11、公司在偿付债务上承担债务责任的财产是()。 A.法人财产 B.出资者财产 C.经营者财产 D.企业全体员工财产 12、某企业按“2/10,n/45”的条件购进商品一批,若该企业放弃现金折扣优惠,而在 信用期满是付款,则放弃现金折扣的机会成本为()。 A、20.99% B.28.82% C.25.31% D.16.33% 13、购买国库券时,不用考虑的风险有()。 A、利率风险 B、再投资风险 C、购买力风险 D、违约风险 14、企业取得短期借款10万元,年利率8%,每季度支付一次利息,则企业负担的实际 利率()。 A.8% B.9% C.8.24% D.2% 15、某企业实际需要筹集资金50万元,银行要求保留20%的补偿性余额,则该企业向 银行借款的总额应为()万元。 A 50 B. 60 C.65 D. 62.5 16、市盈率水平高低,主要取决于()。 A.每股收益 B.资本结构 C.放款信用政策 D.减少利息支出

相关文档

- (完整版)财务管理基础知识点整理

- exam(1) 财务管理基础双语 沈洪涛版本 考试题

- 财务管理基础英文大纲

- 财务管理基础英文版选择题

- 财务管理基础英文课件(1)

- 《财务管理基础第13版》相关章节答案

- 财务管理基础 外文版6PPT课件

- 精品课程财务管理基础-英文课件ch16

- 财务管理基础(英文版)

- 财务管理基础 英文版 选择题.doc

- 精品课程《财务管理基础》英文课件ch(6)

- 财务管理基础(第二版)靳磊第1章 答案

- 精品课程财务管理基础-英文课件ch17

- 精品课程《财务管理基础》英文课件ch(2)

- 企业财务管理基础知识(英文版)

- 财务管理基础 英文版 选择题

- 财务管理基础英文大纲

- 财务管理基础英文版选择题

- 财务管理基础英文大纲

- 精品课程《财务管理基础》英文课件ch(1)